Blog

We keep you up to date on the latest tax changes and news in the industry.

IRA Withdrawal Planning Can Save on Taxes

Article Highlights:

- Early Distributions

- Distributions After Age 59½

- Minimum Required Distributions After Age 72

- Excess Accumulation Penalty

- Estate Tax Issues

Early Distributions (before 59½) - If funds are withdrawn before the taxpayer reaches age 59½, the distribution is subject to a 10% early withdrawal penalty (and state penalties, if applicable) in addition to income taxes, unless what is referred to as the substantially equal payment exemption is utilized. Under this exception, an early retiree can begin taking substantially equal payments at least once a year over their projected lifetime or the joint lives of themself and a designated beneficiary. The payments must not cease before the end of a five-year period beginning with the date of the first payment AND must continue until after the taxpayer reaches age 59½.

Age 59½ to age 72 Distributions – After attaining age 59½, an individual can take funds out of their IRA in whatever amount they wish in any year until reaching age 72. This withdrawal flexibility leaves the retiree to plan their distributions to minimize taxes. Techniques involve matching distributions with no- or low-income years.

Age 72 and Older – Once a taxpayer reaches age 72, they must withdraw at least a minimum amount from their Traditional IRA each year. A taxpayer who fails to take the required minimum distribution (RMD) in the year age 72 is reached can avoid a penalty by taking that distribution no later than April 1st of the following year. However, that means the IRA owner must take two distributions in the following year, one for the year in which they reached age 72 and one for the current year.

When a taxpayer takes distributions that are less than the required minimum distribution for the year, the amount not distributed as required is subject to a 50% excise tax (excess accumulation penalty) for that year. In many cases the excess accumulation penalty can be reduced or totally eliminated by following IRS abatement procedures. Generally, you must show that the failure to take the required distribution was due to reasonable cause and that steps are being taken to remedy the shortfall.

Quite frequently, taxpayers have multiple IRA accounts in addition to one or more types of other retirement plans. This gives rise to a commonly asked question, "Must I take a distribution from each individual account?" For purposes of the annual RMD, a separate distribution must be taken from each type of plan. However, a taxpayer may have multiple accounts for each type of plan, which, for tax purposes, are treated as one plan. For example, if you have three IRA accounts, the three separate accounts are treated as one for tax purposes, and the distribution can be taken from any combination of the accounts.

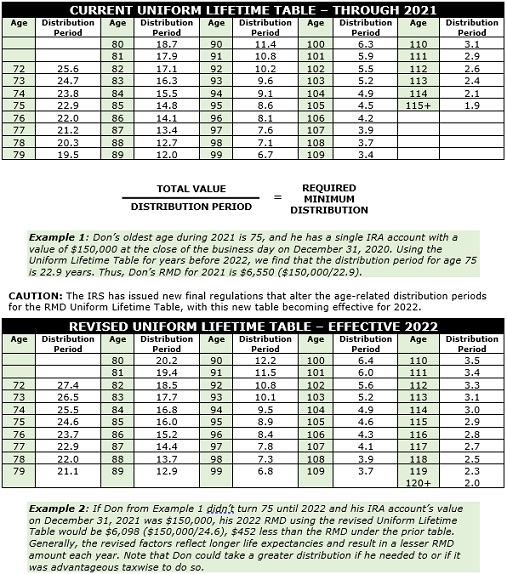

Generally, the minimum amount that must be withdrawn in a particular year, beginning the year a taxpayer reaches age 72, is the total value of all IRA accounts (as determined on December 31st of the prior year) divided by a factor based on the IRA owner’s age. The factor is the estimated remaining life for individuals of that age as determined by the IRS based on longevity studies, and most often, is found in the table below.

Estate and Beneficiary Considerations – When planning your distributions, keep in mind that the value of your undistributed IRA account will be included in your gross estate when you pass on, and depending upon the size of your estate, it may be subject to estate tax. In addition, the inherited IRA distributions will be taxable to the individual who inherits the IRA. Therefore, it could be appropriate for you to utilize your IRA funds first and then dip into other assets after the IRA funds have been depleted. On the other hand, funds left in an IRA do continue to accumulate tax-free, which might be better in certain circumstances. If your spouse is the beneficiary of your IRA, he or she has various options as to holding title to the account and distribution periods, while distribution of the IRA to a non-spouse beneficiary generally will have to be completed no later than ten years after the year of your death.

If you would like assistance with your tax planning needs or to develop an IRA distribution plan, please call this office for an appointment.

Sign up for our newsletter.

Each month, we will send you a roundup of our latest blog content covering the tax and accounting tips & insights you need to know.

We care about the protection of your data.

“We are always looking to grow our business. Should you have any clients, friends, business associates looking for high quality accounting services from a CPA firm, please have them contact us.”

This e-mail (including any attachments) is only for the exclusive use of the individual to whom it is addressed. The information contained hereinafter may be proprietary, confidential, privileged and exempt from disclosure under applicable law. If the reader of this e-mail is not the intended recipient or agent responsible for delivering the message to the intended recipient, the reader is hereby put on notice that any use, dissemination, distribution or copying of this communication is strictly prohibited. If the reader has received this communication in error, please immediately notify the sender by telephone or e-mail and delete all copies of this e-mail and any attachments.

IRS Circular 230 Disclosure: In order to ensure compliance with IRS Circular 230, we must inform you that any U.S. tax advice contained in this transmission and any attachments hereto is not intended or written to be used and may not be used by any person for the purpose of (i) avoiding any penalty that may be imposed by the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any tax-related matter(s) addressed herein.